Year-End Accounting Checklist: A Practical Guide for Finance Teams

December can be one of the busiest months of the year. Between the holiday sales rush, team members taking time off, and looming deadlines, the winter months bring more stress than usual. On top of it all, the end of the year is when businesses need to complete their year-end accounting, an arduous task made even more difficult without the right tools and a solid plan.

The year-end close process serves two purposes. First, it ensures all your reports, financial statements, and outstanding liabilities are accurate and ready to present to the IRS and relevant state agencies. Second, it is your opportunity to get everything in order so you can start Q1 on the right foot. Any oversight now can turn into a costly mistake later, which is why the end of the year is prime time for internal audits, financial analysis, and cleanup of your books.

In this guide, we’ll walk through the 12 steps involved in the year-end close process. We’ll share best practices, explain how different business models should approach certain accounting processes, and break down key tax and financial management considerations.

We will also show how using a business banking platform like Slash can help you stay better prepared and make your year-end close far more efficient. With Slash, every transaction across your cards and accounts is tracked, categorized, and ready to sync with your accounting system.¹ You can also set granular spend controls for your team so they stay compliant, reducing the risk of surprises when it is time to review your books.

What Happens During Year-End Accounting Close?

Your year-end accounting close is a comprehensive review of your financial activity across the entire year. While many of these processes happen on a monthly basis, the year-end close is much more detailed; it’s also directly tied to tax reporting and long-term planning. Here are the core accounting procedures involved:

- Account reconciliation: This is the process of matching your internal records against external statements, such as bank accounts, credit cards, and payment processors.

- Categorizing and cleaning up transactions: Every transaction should be properly categorized into the correct expense or revenue account.

- Reviewing financial statements: You will generate and review key reports like your income statement, balance sheet, and cash flow statement.

- Recording adjusting entries: Adjusting entries account for income and expenses that have been earned or incurred but not yet recorded. This includes things like accrued expenses, deferred revenue, depreciation, and amortization.

- Accounts payable and receivable review: You will review outstanding invoices you owe and payments you are owed. This includes confirming balances, writing off uncollectible receivables if necessary, and ensuring liabilities are properly recorded.

- Inventory and asset checks: If your business holds inventory or fixed assets, you will verify physical inventory counts, value assets, and record depreciation.

- Financial analysis and performance review: The year-end close is a chance to evaluate your business’s performance. You will analyze profitability, margins, spending patterns, and cash flow trends to inform budgeting and strategy for the next year.

Once everything is reviewed and finalized, you formally close your books for the year. This prevents further changes and locks in your financial data for reporting and compliance purposes.

Accounting methods and timing

Your year-end close will look slightly different depending on your accounting method, which determines when income and expenses are recorded. Most businesses use either cash-basis or accrual accounting

With cash-basis accounting, transactions are recorded only when cash is received or paid. You count income when it hits your bank account and expenses when you pay them. This makes things more straightforward, but at year end, timing becomes important. For example, you might choose to pay certain expenses before December 31 or delay collecting income until January, depending on how you want your finances to appear for the year.

With accrual accounting, revenue and expenses are recorded when they are earned or incurred, regardless of when cash changes hands. For example, if you send an invoice in December but get paid in January, that income still counts for December. This method gives a more accurate picture of your business, but it also means you need to make extra adjustments at year end to account for things like unpaid invoices, upcoming expenses, or revenue you have not yet fully earned.

Common Year-End Accounting Challenges

A smooth year-end close depends heavily on the habits you build throughout the year and the tools you use to support them. Here are some of the most common challenges to watch for. If you encounter any of them, it may be a sign your accounting processes need an upgrade:

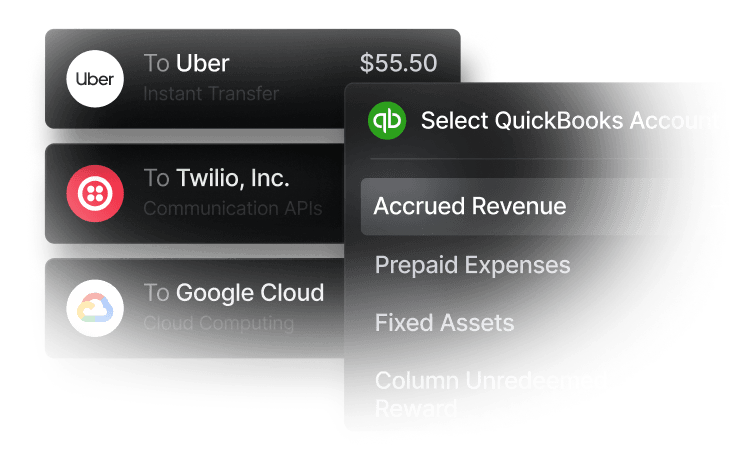

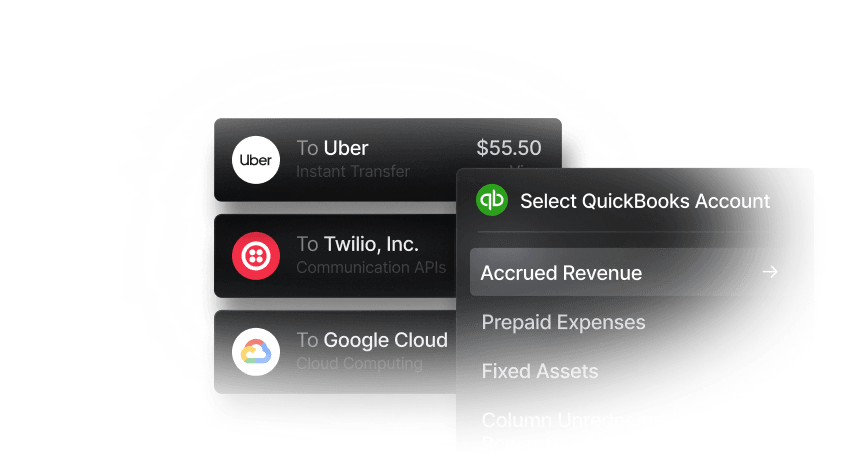

- Incomplete or missing records: When transactions are spread across cards, accounts, and tools, it is easy for things to slip through. Using a platform like Slash ensures every transaction is captured in one place automatically, so you are not chasing down missing records at year end.

- Unreconciled accounts: Discrepancies between your books and statements can build up over time, especially if reconciliations are delayed.

- Misclassified transactions: Manual categorization is time-consuming and prone to error, especially at scale. Slash can automatically categorize transactions, reducing the amount of cleanup needed before closing your books.

- Disconnected systems and manual syncing: Pulling data from multiple platforms and uploading it into your accounting software can slow down the close. Slash integrates directly with your accounting tools, keeping your financial records up to date without manual work.

- Last-minute adjustments and time pressure: When monthly accounting processes are put off, year-end can turn into a scramble. Waiting until the last minute to organize your finances can increase the likelihood of missed details and make the close more stressful overall. That’s why it’s important to rely on consistent, monthly reviews prior to the end of the year.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

The 12-Step Year-End Accounting Checklist

1. Gather and organize financial documents

The first step in the year-end close is making sure you have a complete record of the year. That means pulling together all relevant financial documents in one place:

- Bank statements

- Credit card statements

- Receipts and expense records

- Bills and invoices

- Payroll reports

- Loan statements

- Sales tax records

- Fixed asset purchase documentation

- Prior tax filings

If your business uses multiple systems, such as a bookkeeping platform, payroll provider, ecommerce platform, or payment processor, this is also the point where you make sure those records line up and nothing is missing.

At the end of the year, this step matters more than it does during a normal monthly close because the goal is not just to keep your books current. It is to finalize them. Missing documentation can delay your close, create issues during tax filing, or cause problems in an audit.

2. Reconcile all bank and credit card accounts

Reconciliation means comparing the transactions in your books against your actual account statements and confirming that they match across:

- Bank accounts

- Credit cards

- Loan accounts

- Payment processors (Stripe, PayPal, Shopify, etc.)

By the end of the reconciliation process, you should understand every difference between your books and your statements. Common items to review include checks that have not cleared, deposits in transit, missing transactions, or duplicate entries.

Pay close attention to timing differences around late December, such as deposits in transit or charges that post in early January, and confirm that anything unusual has a clear explanation. If you are managing multiple accounts or cards, this is also a good point to make sure nothing has been overlooked across systems.

3. Review and categorize all transactions

Once transactions are confirmed as complete, they need to be reviewed for proper classification. This includes making sure:

- Income is posted to the correct revenue accounts.

- Expenses are mapped to the right categories.

- Transfers are not incorrectly recorded as income.

- Balance sheet items are not misclassified as expenses.

- Uncategorized or unclear transactions are resolved.

Your tax return depends on how transactions are categorized, so errors here can lead to missed deductions or incorrect reporting. Common problem areas include software spend, contractor payments, meals, travel, loan payments, and equipment purchases.

4. Process outstanding invoices and accounts receivale

At year end, accounts receivable needs a closer review than usual. Start by identifying:

- All open customer invoices

- Aging balances by customer

- Disputed or delayed payments

- Invoices that may be uncollectible

You may need to follow up on collections, resolve billing issues, or decide whether certain invoices should be written off.

For accrual-basis businesses, this step matters because income is recorded when earned, not when cash is received. Reviewing receivables at year end helps ensure your reported revenue aligns with what you reasonably expect to collect.

5. Verify accounts payable and outstanding bills

Next, take a close look at everything your business owes as of year end. This includes:

- Unpaid vendor invoices

- Recurring subscriptions

- Employee reimbursements

- Loan balances and interest

- Accrued expenses not yet billed

At year end, the focus is on cutoff and accuracy. You want to confirm that expenses are recorded in the correct period, even if invoices have not been received yet; that may require reviewing vendor agreements and recurring services to identify costs tied to December that need to be accrued. It is also a good time to validate large or unusual expenses and make sure they are classified correctly.

For accrual accounting, this ensures expenses are not understated. For cash-basis businesses, it helps inform whether to pay certain bills before year end to capture deductions or defer them to manage cash.

6. Calculate and record depreciation

If your business purchased long-term assets during the year, you will need to review and update your fixed asset records. Instead of expensing these purchases all at once, they are typically spread out over time through depreciation.

At year end, you will confirm which assets were placed in service and calculate how much of their cost should be recognized as an expense for the current year. This is based on the asset’s useful life and the depreciation method you are using. Getting this right ensures your expenses and profits are not overstated or understated in any given period.

This step also has important tax implications. While financial reporting usually spreads depreciation over several years, tax rules may allow you to accelerate deductions through provisions like Section 179 or bonus depreciation. The right approach depends on your business and can have a meaningful impact on your taxable income for the year.

7. Conduct physical inventory counts (if applicable)

If your business holds inventory, year end is the time to validate what you actually have on hand. Start by conducting a physical count and comparing those results to your recorded inventory levels. From there, reconcile any discrepancies and investigate gaps caused by shrinkage, returns, or timing issues. You should also identify damaged or obsolete goods that may need to be written down and confirm balances across any warehouses or third-party fulfillment partners.

Retail, ecommerce, and wholesale businesses should pay close attention here, particularly if inventory is spread across multiple locations or managed externally. You will also need to ensure your inventory valuation method is applied consistently, since it directly impacts both reporting accuracy and your tax position.

8. Review payroll records and tax forms

Payroll should be reviewed before the year closes to make sure everything is accurate and complete. That includes confirming that wages, bonuses, contractor payments, and benefits have been recorded correctly, and that tax withholdings and employer payroll taxes align with your filings.

Year end is also when payroll reporting is finalized. You will prepare required forms for employees and contractors and double check that payment totals and identifying information are correct.

If you have employees or contractors in multiple states, this is a good time to make sure everything lines up across jurisdictions so there are no surprises when filings are due.

9. Make necessary adjusting entries

Adjusting entries are used to finalize your books by recording activity that has not yet been captured. Common year-end adjustments include:

- Accrued expenses or payroll

- Prepaid expenses

- Deferred revenue

- Earned but unbilled revenue

- Depreciation and amortization

- Interest expenses

This is where year-end accounting becomes more detailed than your normal monthly process. Many businesses rely on estimates or simplified entries during the year, then finalize them at year end. These adjustments can significantly impact your reported profit, so they should be reviewed carefully and supported with documentation.

10. Prepare financial statements

Once your books are reconciled and adjusted, you can generate your year-end financial statements: your income statement, balance sheet, and cash flow statement. These reports are the final output of your close and will be used for tax filing, reporting, and planning.

11. Backup all your financial data

Before closing the year, make sure your financial records are securely backed up and easy to access. The goal is to create a clean, complete record of your books and supporting documents. This will save time if you need to reference past data, share it with a CPA, or respond to an audit.

12. Plan for tax filing

With your books finalized, you can move into tax preparation with a clear and accurate set of financials. At this stage, the focus is on making sure your reporting aligns with tax requirements. That includes confirming income and expense treatment, reviewing any book-to-tax differences, and ensuring all necessary documentation is in place for your CPA or internal team. If you operate across multiple states or jurisdictions, this is also where you confirm filing requirements and obligations.

A clean year-end close should make this process straightforward. It gives you confidence that your filings are based on complete, well-documented numbers and reduces the risk of adjustments, delays, or follow-up questions later.

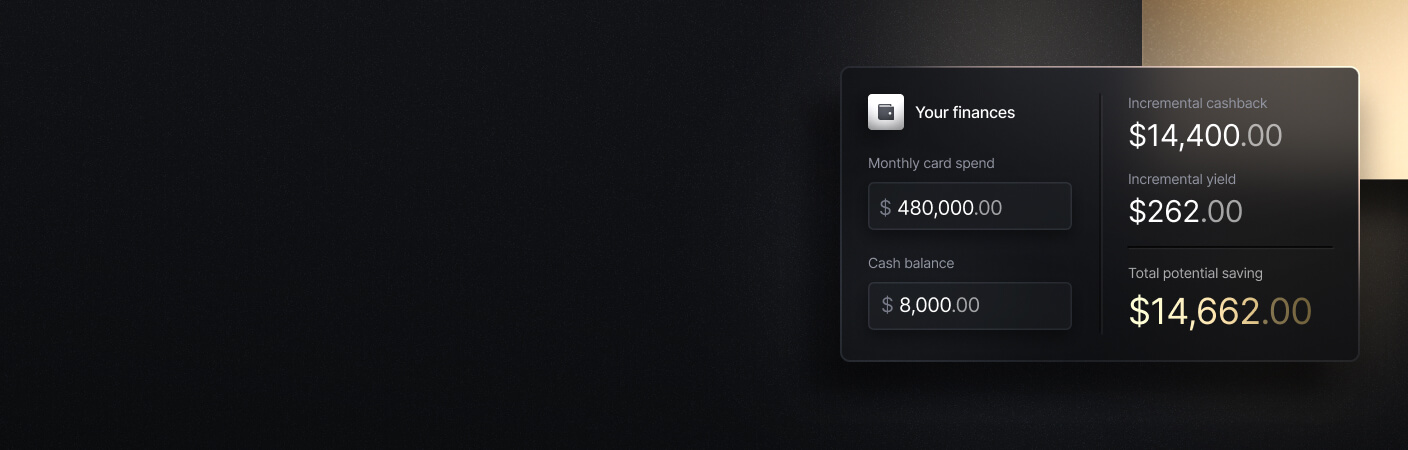

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

Preparing for Next Year: Strategic Planning Tips

During the year-end close process, you may have encountered some of the challenges we mentioned earlier in the article: slow, manual accounting processes; inaccuracies in your ledger; or a mountain of paperwork from missed financial reviews throughout the year. If your close felt more difficult than it should have, there is likely room to improve. Consider implementing these changes to simplify things for next year:

- Standardize your monthly close: If year-end felt heavy, it may have been because much of your monthly accounting work was deferred. Building a consistent monthly close process, including reconciling, categorizing, and reviewing your books will likely make next year’s close far more manageable.

- Refine your expense categories and chart of accounts: If you found yourself reclassifying hundreds of transactions or struggling to understand where money was going, it may be time to simplify or restructure your chart of accounts so reporting is clearer.

- Revisit your accounting setup: If your current system slowed down your close, it may be time to upgrade. Moving to an accounting software like Xero or QuickBooks or an ERP platform like Sage Intacct or NetSuite can help automate processes and keep your books clean throughout the year.

- Automate where possible: If your close relied heavily on manual work, consider tools like Slash that can automate transaction tracking, categorization, and reconciliation to reduce errors and save time throughout the year.

- Adjust internal controls and spending policies: Establish clearer rules around approvals, reimbursements, and team spending to prevent issues before they show up in your books.

How Slash Can Streamline Your Year-End Accounting Process

A smooth year-end close starts with clean, consistent financial data. Most of the work comes down to staying organized, keeping records up to date, and reducing the amount of manual cleanup required at the end of the year. The tools you use play a direct role in how manageable that process is.

With Slash, you can:

- Sync directly with your accounting software: Two-way integrations with QuickBooks, Xero, and Sage Intacct ensure your financial data stays aligned without manual uploads or duplicate work.

- Access real-time financial data: Up-to-date transaction data means you are not waiting until month or year end to understand your financial position.

- Automate categorization and reporting: Transactions are automatically categorized and synced to your ledger, reducing errors and minimizing cleanup during your close.

- Track invoices and outstanding payments: Built-in invoice management helps you track outstanding balances and keep receivables accurate.

- Manage multiple accounts in one place: Whether you have multiple entities, teams, or accounts, Slash gives you a centralized view so nothing gets overlooked during reconciliation.

Set yourself up for a smoother close next year. Use Slash to keep your financial data organized, accurate, and in sync from the start.

Apply in less than 10 minutes today

Join the 10,000+ businesses already using Slash.

This content is for informational purposes only and does not constitute legal, tax, or accounting advice. You should consult with a qualified professional for advice specific to your business.

Frequently Asked Questions

When should I start my year-end accounting process?

You should start preparing in early December, or even late November, especially for gathering documents and cleaning up transactions. The more you handle before year end, the smoother and faster your final close will be.

What documents do I need for year-end accounting?

You will need all financial records from the year, including bank and credit card statements, receipts, invoices, payroll reports, loan statements, and tax documents. If you use multiple systems, you should also pull reports from each.

Expense Reports: How to Track, Manage, and Simplify Costs

The Complete Guide to LLC Expenses and Tax Deductions

How can I speed up my year-end process?

Keeping your books up to date throughout the year is the biggest factor. Regular reconciliations, consistent categorization, and using tools like Slash that automate tracking and syncing can significantly reduce the amount of cleanup needed at year end.

The Best Accounting Automation Software Tools in 2026

Do I need an accountant for year-end closing?

Not necessarily, but many businesses may benefit from having an accountant review their books or handle tax preparation.

Bookkeeping For Startups: Setup & Best Practices